Marine insurance often confuses shipowners, charterers, and cargo owners because each policy covers different risks. The three most common forms—Hull & Machinery, Cargo, and P&I insurance—are essential in global trade. This article gives you a quick comparison and explains their core differences.

1. Quick Comparison

Before diving into details, the following table shows the main differences between Hull & Machinery, Cargo, and P&I insurance.

| Aspect | Hull & Machinery | Cargo Insurance | P&I Insurance |

|---|---|---|---|

| Subject insured | Vessel and its machinery | Goods in transit | Third-party liabilities |

| What it covers | Damage to hull, engines, collision, breakdown | Loss, theft, or damage to cargo | Crew injury, pollution, cargo claims, collisions |

| Exclusions | Wear & tear, poor maintenance | Poor packaging, delay, inherent defects | Illegal acts, certain war risks |

| Who needs it | Shipowners & operators | Cargo owners, shippers, traders | Shipowners, charterers |

| Example claim | Repair after collision | Cargo spoiled by seawater | Compensation for oil spill |

Key takeaways:

- Hull & Machinery covers the vessel itself.

- Cargo insurance protects goods in transit.

- P&I covers third-party liabilities and legal claims.

- Shipowners usually need both H&M and P&I, while cargo owners need cargo insurance.

2. Hull & Machinery Insurance in Brief

Hull & Machinery insurance (H&M) is designed to protect the physical asset of the ship. It focuses on safeguarding the vessel’s structure and engines against unexpected risks.

Covers physical damage to the vessel and machinery

H&M provides compensation if the ship’s hull, engines, or machinery are damaged. Typical scenarios include collision with another vessel, grounding, fire, or storm damage. This ensures that shipowners can repair or restore the vessel without bearing the full cost.

Key buyers: shipowners

The main buyers of H&M are shipowners and operators, since the ship itself is their primary investment. Without this cover, a single accident could create financial losses larger than the vessel’s value.

Typical claim: collision damage or machinery breakdown

For example, if a vessel collides with a pier and suffers a cracked hull, H&M covers repair costs. Similarly, if a critical engine part breaks during a voyage, the policy helps pay for replacement.

3. Cargo Insurance in Brief

Cargo insurance is focused on protecting the goods transported by sea, whether for traders, exporters, or importers. It is often mandatory in international shipping contracts.

Covers goods in transit against risks

Cargo insurance protects shipments from perils such as fire, theft, seawater damage, or loss during loading and unloading. It ensures that the cargo owner does not bear the financial burden when goods are lost or damaged.

Key buyers: cargo owners, shippers, traders

The buyers of cargo insurance are usually the owners of goods, not the vessel itself. For example, an exporter of electronics wants to make sure the products are safe until delivery to the buyer.

Typical claim: cargo damaged by seawater during voyage

If a container of textiles gets wet during a storm and the goods arrive in poor condition, cargo insurance covers the financial loss. This helps traders maintain business continuity without disputes over compensation.

4. P&I Insurance in Brief

Protection & Indemnity (P&I) insurance is different from Hull & Machinery or Cargo because it focuses on third-party liabilities. It is usually provided by P&I Clubs, which are mutual associations of shipowners.

Covers third-party liabilities

P&I covers risks such as crew injury, passenger claims, pollution, wreck removal, and liability for damage to another vessel or its cargo. These are high-cost risks that cannot be covered fully by Hull & Machinery or Cargo policies.

Key buyers: shipowners, charterers

The main buyers of P&I are shipowners and charterers who need protection against claims from third parties. Without P&I, even a single pollution claim could reach millions of dollars and endanger the company’s survival.

Typical claim: compensation for oil spill or crew injury

For example, if a vessel accidentally releases oil into the sea, P&I covers cleanup costs and third-party claims. Similarly, if a crew member suffers an injury onboard, the shipowner’s liability is handled by the P&I policy.

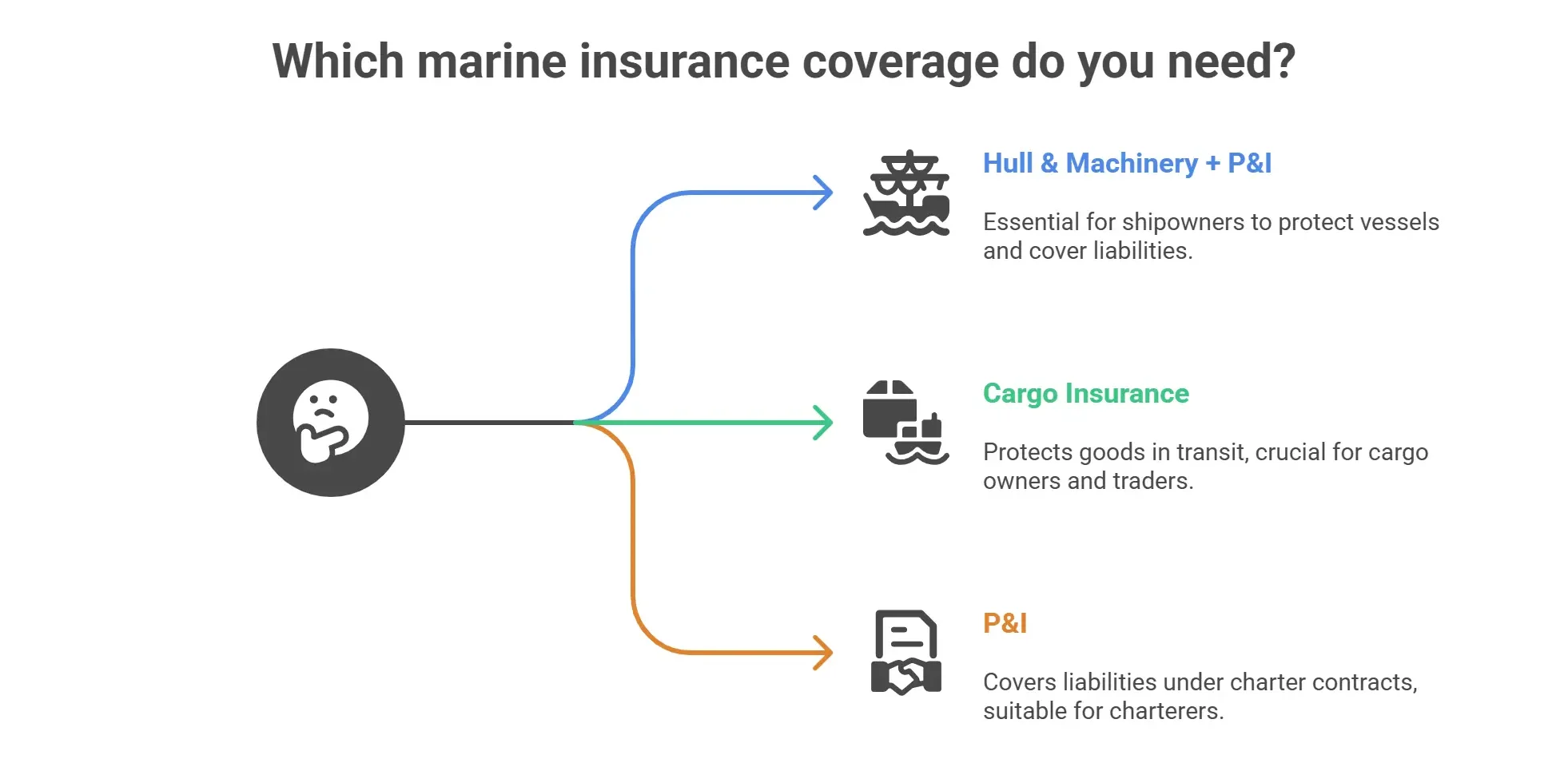

5. Which Coverage Do You Need?

Each of the three types of insurance addresses a different risk. The right choice depends on whether you own the vessel, transport goods, or manage liabilities.

Shipowners: Hull & Machinery + P&I

Shipowners typically need both Hull & Machinery (to protect the ship) and P&I (to cover third-party risks). Without this combination, they face serious gaps in protection.

Cargo owners and traders: Cargo insurance

For exporters, importers, or traders, cargo insurance is essential. It ensures their goods are financially protected during international shipping, even if the shipowner already has other covers.

Charterers: P&I and sometimes cargo insurance

Charterers may be responsible for third-party liabilities under charter contracts, making P&I necessary. In some cases, they also purchase cargo insurance depending on the terms of the agreement.

6. Final Thoughts

Hull & Machinery, Cargo, and P&I insurance each play a unique role in maritime risk management. Together, they create a safety net that protects ships, goods, and liabilities.

In practice, no single policy is enough. A balanced mix of Hull & Machinery, Cargo, and P&I insurance ensures that both physical assets and financial liabilities are covered. By choosing the right combination, shipowners, traders, and charterers can safeguard their operations and reduce the risks of global shipping.