Charterer liability insurance protects charterers from financial losses arising from their legal responsibilities during vessel use. In this guide, you’ll learn what it covers, why it’s essential, and how to choose the right policy.

Below is a Summary Table of Coverages and Risks. It has four columns:

- Risk Type: The category of potential loss

- Coverage Description: What the charterer liability policy covers

- Example: A real-world illustration of the risk

- Why It Matters: The practical importance of each coverage

| Risk Type | Coverage Description | Example | Why It Matters |

|---|---|---|---|

| Damage to Vessel | Repair costs and legal expenses | Hull damage during cargo operations | Prevents out-of-pocket payments to the shipowner |

| Pollution Liability | Cleanup costs and government fines | Bunker spill at port | Covers environmental penalties and remediation expenses |

| Delay & Demurrage | Compensation for demurrage and off-hire penalties | Six-day idle time due to berth unavailability | Protects against costly vessel downtime charges |

| Cargo Liability & Misdelivery | Compensation to cargo owners and legal defense | Grain contamination during loading | Ensures client satisfaction and avoids cargo claims |

| Charter Party Breach | Legal dispute costs and contractual damages | Early redelivery or deviation from agreed route | Covers contractual disputes and accelerates resolution |

1.What Is Charterer Liability Insurance?

Charterer liability insurance is a critical component of marine risk management, tailored specifically for individuals or entities that charter vessels. The following sections explain what this coverage entails and how it differs from other types of marine insurance.

Definition and Purpose of Charterer Liability Insurance

Charterer liability insurance is a specialized marine policy that covers the legal liabilities of a charterer arising from the use of a vessel they do not own. It protects against risks such as vessel damage, pollution, cargo loss, and third-party claims — all of which may stem from the charterer’s operational control under a charter party agreement.

This insurance becomes particularly vital when the charterer assumes responsibilities that could trigger financial loss or legal disputes, even if they are not directly involved in the ship’s navigation or maintenance.

How It Differs from Other Marine Insurance Types

Charterer liability insurance is often confused with Hull & Machinery (H&M) and Protection & Indemnity (P&I) insurance. However, its scope is distinctly focused on the charterer’s liabilities, not the shipowner’s.

Key distinctions include:

- H&M covers physical damage to the vessel — for the owner.

- P&I protects shipowners from third-party liabilities (e.g., crew injury, pollution).

- Charterer liability insurance fills the gap by protecting charterers from legal and financial consequences tied to their use of the vessel.

Why Charterers Need Specialized Liability Coverage

Charterers often underestimate their exposure to legal claims, especially when using third-party vessels. However, they can be held accountable for numerous events, including cargo mishandling, loading delays, pollution fines, and breaches of charter agreements.

Main reasons charterers need this coverage:

- To safeguard against unpredictable maritime claims.

- To fulfill contractual requirements under many charter parties.

- To avoid costly litigation and business interruption.

This tailored policy gives peace of mind and financial security, especially in complex global shipping environments.

2.Who Needs Charterer Liability Insurance?

Charterer liability insurance is not mandatory in all jurisdictions, but it’s highly recommended for any party taking responsibility for vessel use, even for a single voyage. The level of exposure depends on the type of charter and the charterer’s role in operations.

Voyage Charterers

Voyage charterers hire vessels for a specific journey and pay based on cargo carried or distance sailed. They do not control the crew or daily operations but are still liable for issues like:

- Poor cargo loading practices

- Delay penalties or demurrage

- Cargo loss during the voyage

Even with limited control, voyage charterers can face legal claims, especially under cargo and charter party clauses.

Time Charterers

Time charterers rent vessels for a defined period and often manage bunkering, scheduling, and port selection. They are more operationally involved and therefore face greater liability risks.

Typical risks for time charterers include:

- Pollution fines during bunkering operations

- Cargo misdelivery or late delivery

- Off-hire disputes with owners

Because they operate the vessel without owning it, time charterers need strong protection against third-party and vessel-related liabilities.

Bareboat/Demise Charterers

Bareboat charterers effectively operate as vessel owners. They hire the crew, manage maintenance, and assume full legal and operational responsibility. In this case, their exposure is highest among all charterer types.

Insurance is crucial here not only to cover liabilities but also to satisfy legal and financial compliance standards expected of ship operators.

Traders, Operators, and Freight Forwarders

Entities that charter vessels for transporting their own or clients’ goods—like commodity traders or logistics companies—also qualify as charterers under legal definitions. Even if they outsource operations, their role in the charter agreement exposes them to liability.

Whether managing one voyage or an entire fleet, these parties need charterer liability insurance to protect against operational, contractual, and regulatory risks.

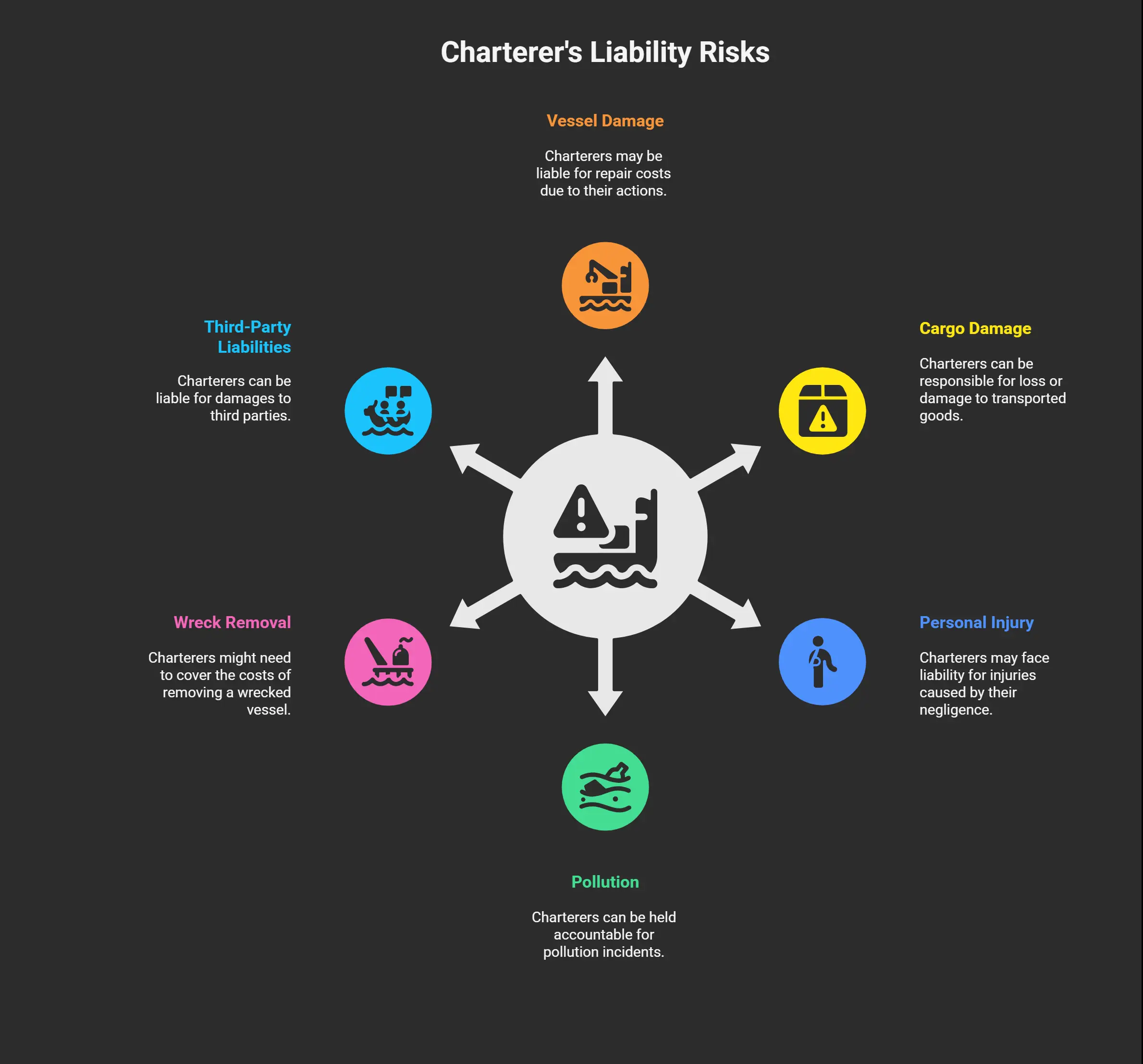

3.What Does Charterer Liability Insurance Cover?

This type of insurance offers broad coverage tailored to the charterer’s responsibilities. It acts as a financial buffer against common liabilities that arise in maritime operations.

Damage to the Vessel (e.g., hull damage due to stevedore operations)

If a vessel is damaged due to poor loading techniques, faulty equipment, or stevedore errors arranged by the charterer, the shipowner may seek compensation. Charterer liability insurance covers repair costs and legal expenses arising from such incidents.

Cargo Liability and Misdelivery

Cargo-related claims—such as spoilage, contamination, theft, or misdelivery—can be directed at the charterer if they were responsible for cargo handling or instructions. Insurance helps cover:

- Compensation to cargo owners

- Legal defense against claims

- Costs of investigating the incident

Pollution Liability

Environmental regulations are strict, and pollution incidents—especially oil spills—can result in large fines and cleanup expenses. If bunkering, ballast operations, or discharges occur under the charterer’s instruction, liability falls on them. This insurance provides:

- Coverage for cleanup costs

- Government-imposed fines (non-criminal)

- Legal representation

Fines and Penalties

Authorities can impose penalties for various breaches, such as:

- Non-compliance with port documentation

- Breach of customs or quarantine laws

- Failure to follow emission regulations

Charterer liability insurance can reimburse these fines, as long as the action wasn’t willful or criminal in nature.

Delay Damages and Off-Hire Claims

Delays caused by charterer actions—such as slow loading, miscommunication, or lack of readiness—can result in contractual penalties. The policy may cover:

- Delay-related fines or demurrage

- Off-hire compensation to owners

- Losses due to idle vessel time

Damage to Third Parties

If third parties, such as port workers or terminal operators, are injured due to the charterer’s directions or negligence, the charterer can be held responsible. Insurance helps manage:

- Medical or compensation claims

- Lawsuits from affected parties

- Settlement or legal costs

Charter Party Breach Costs

A breach of the charter agreement—such as non-payment, early redelivery, or deviation from the agreed route—can trigger costly legal disputes. Insurance often includes legal assistance and compensation for such contractual claims.

Salvage, Towage, and General Average Contributions

In maritime emergencies, if the vessel is towed or salvaged due to a situation caused by the charterer’s fault (e.g., grounding, cargo fire), the charterer may need to contribute to the cost. The policy helps cover:

- Salvage operation costs

- Emergency towage

- Charterer’s share in general average

✅Why this matters: These coverage items address real-world scenarios that can cripple operations without insurance. Whether you’re chartering for a day or a year, these risks apply.

4.Key Exclusions in Charterer Liability Insurance

While charterer liability insurance offers broad protection, it does not cover every possible risk. Understanding these exclusions is crucial to avoid costly surprises during a claim.

Acts of War or Terrorism

Most policies exclude coverage for liabilities arising from acts of war, armed conflict, or terrorism. These are considered high-risk, politically driven events and are typically insured under separate war risk policies. If a vessel is attacked or damaged in a conflict zone, the charterer would not be covered unless additional war coverage has been purchased.

Gross Negligence or Misconduct

Intentional acts or gross negligence—such as knowingly violating safety procedures or failing to report critical damage—are not covered. Insurers expect charterers to operate within a standard of due diligence. If reckless or illegal behavior leads to a loss, the claim is likely to be denied.

Examples of misconduct that void coverage include:

- Instructing a vessel to sail in prohibited waters

- Ignoring known cargo incompatibility

- Falsifying documentation

Fines Due to Willful Violation of Laws

While unintentional breaches may be covered, fines resulting from deliberate violations of international regulations, such as MARPOL or SOLAS, are usually excluded. For example, if a charterer orders illegal discharge of waste to reduce costs, any resulting fines or clean-up expenses will be the charterer’s responsibility.

Coverage Gaps Between Policies (e.g., overlap with P&I or H&M)

Charterer liability insurance does not duplicate coverage provided by other marine insurance policies. If a claim falls within the shipowner’s P&I or H&M policy scope, the charterer’s policy may not respond.

Common examples of gray areas:

- Machinery failure caused by shipowner negligence (not the charterer’s fault)

- Crew injury (typically under P&I)

- Hull damage not related to cargo operations

✅Why it matters: Understanding exclusions helps charterers identify gaps and either negotiate additional endorsements or purchase supplementary insurance.

5.Charterer Liability vs. P&I and Hull Insurance

Charterer liability insurance often overlaps in concept with other marine policies. However, each serves a different purpose and applies to different parties involved in maritime operations.

What P&I Covers vs Charterer Liability

Protection & Indemnity (P&I) insurance is mainly for shipowners. It covers third-party liabilities such as crew injuries, environmental pollution, and collision damages. However, it doesn’t cover a charterer’s liabilities unless they are an entered member of a P&I Club, which is rare.

Charterer liability insurance, by contrast, focuses on the liabilities faced by the charterer, particularly those arising from the charter party, such as:

- Misdelivery of cargo

- Pollution due to charterer-instructed bunkering

- Fines from cargo misdeclaration

Role of Hull & Machinery (H&M) Insurance

Hull & Machinery insurance covers physical damage to the ship itself and is owned by the shipowner. It pays for repairs or loss if the vessel is damaged in accidents such as grounding, fire, or collision.

If a charterer causes hull damage due to faulty loading operations or mismanagement of cargo equipment, they may be liable — and that’s where charterer liability insurance steps in to reimburse the shipowner.

Where Charterer Liability Fills the Gap

Many liabilities don’t fall clearly into P&I or H&M. Charterer liability insurance fills these gaps by covering:

- Contractual breach claims

- Demurrage and off-hire penalties

- Stevedore damage during charterer-controlled loading

- Third-party injury under charterer operations

Example: If a ship is delayed because a time charterer failed to secure a berth on time, H&M and P&I won’t respond — but charterer liability insurance might.

Why Relying on the Shipowner’s Insurance May Not Be Enough

It’s a common misconception that the shipowner’s insurance will protect everyone involved. However, shipowners’ policies are designed to protect their own interests, not the charterer’s. Relying solely on them leaves the charterer exposed to:

- Cross-claims from the shipowner

- Contractual penalties not covered under P&I

- Cargo claims due to charterer mismanagement

✅ Quick Comparison Table:

| Insurance Type | Who It Covers | Main Purpose |

|---|---|---|

| P&I | Shipowners | Third-party liability (crew, cargo, oil) |

| Hull & Machinery (H&M) | Shipowners | Physical damage to the vessel |

| Charterer Liability | Charterers | Operational and contractual liabilities |

Understanding the difference ensures you’re not underinsured — or worse, uninsured — for liabilities that directly affect your financial exposure as a charterer.

6.How to Choose the Right Charterer Liability Policy

Choosing the right policy is more than just selecting a premium. It requires evaluating your operations, risk profile, and charter party terms to ensure you’re covered for the most likely and costly risks.

Assessing Your Charter Type and Risk Exposure

Different charter types (voyage, time, bareboat) carry different liabilities. For instance, a bareboat charterer assumes full control and thus needs more comprehensive coverage than a voyage charterer who only manages one shipment.

Risk factors to assess:

- Frequency of charters

- Type of cargo (e.g., hazardous, refrigerated)

- Geographic regions (e.g., war zones, high-traffic ports)

- Level of operational control (fueling, scheduling, loading)

Understanding your unique profile helps tailor a policy that fits your real exposure.

Key Clauses to Look For in a Policy

The policy wording can significantly affect how claims are handled. Carefully review clauses related to:

- Pollution liability limits

- Cargo damage exclusions

- Charter party breach coverage

- Fines and penalties reimbursement

- Territorial limits and applicable law

A specialist marine insurance broker can help interpret ambiguous terms and ensure no critical gaps are overlooked.

Choosing the Right Limit and Deductible

Selecting policy limits is a balancing act. Too low, and you risk underinsuring. Too high, and premiums may become unnecessarily expensive. Deductibles (excess amounts paid out-of-pocket) also affect pricing.

General guidance:

- Set limits based on worst-case claim scenarios

- Choose deductibles you can reasonably afford in a crisis

- Consider increasing limits if operating globally or in high-risk sectors

Working with Brokers and Marine Underwriters

Marine insurance is a specialized field. Partnering with brokers who understand maritime operations ensures you get access to the best coverage terms and carriers. They can also help negotiate rates, recommend reputable underwriters, and support you during claims.

Look for brokers who:

- Work with P&I Clubs and international marine insurers

- Have experience with charter party contracts

- Offer comparative policy reviews

Role of Legal Advice in Charter Party Terms

Legal review of your charter party contract is crucial. Many liability claims arise from unclear or unfavorable clauses. Your lawyer should ensure:

- Clear division of responsibilities

- Proper indemnity wording

- Insurance obligations matched with actual coverage

✅ Why it matters: An ideal insurance policy works hand-in-hand with your contracts and operations. A mismatch between them can lead to denied claims or major financial exposure.

7.Cost of Charterer Liability Insurance

The cost of charterer liability insurance varies widely depending on several operational and risk-based factors. This section outlines what influences premiums and how charterers can manage costs effectively.

Factors That Influence Premium Pricing

Insurers assess multiple elements to determine a charterer’s premium. Understanding these variables can help you estimate and control your insurance budget.

Key factors include:

- Type of Charter: Bareboat charters usually carry higher premiums due to full operational responsibility.

- Vessel Size and Type: Larger ships or specialized vessels (e.g., tankers, LNG carriers) incur higher premiums.

- Cargo Type: Hazardous, temperature-sensitive, or high-value cargo increases risk.

- Trading Area: Operating in war zones or congested ports increases liability exposure.

- Loss History: A history of frequent or high-value claims results in higher pricing.

Insurers also consider policy limits and deductibles — higher limits cost more, but may offer better protection depending on your risk tolerance.

Example Quotes Based on Vessel Size and Type

While actual premiums vary by underwriter, the table below offers ballpark figures for time charter operations with standard coverage limits:

| Vessel Type | Average Annual Premium (USD) |

|---|---|

| Handymax Bulk Carrier | $7,000 – $12,000 |

| Aframax Tanker | $15,000 – $25,000 |

| Container Ship (2500 TEU) | $10,000 – $18,000 |

| LNG Carrier | $30,000 – $50,000 |

These estimates are for policies with coverage limits around $10M and deductibles of $25,000–$50,000. Premiums can be significantly lower for short-term voyage charters or higher-risk routes.

Additional Costs: War Risks, COFR, Pollution Surcharge

In certain cases, base charterer liability insurance is not enough, and charterers may need to purchase extra coverage or endorsements:

- War Risk Insurance: Required when sailing through conflict zones.

- COFR (Certificate of Financial Responsibility): Mandated by U.S. law for pollution liability in U.S. waters.

- Pollution Surcharge: Additional premium for operations involving high-risk fuels or bunkering activities.

These costs are usually not included in the main policy and must be quoted separately.

How to Reduce Insurance Costs with Risk Management

Effective operational practices can help lower premiums over time. Insurers reward charterers who demonstrate strong risk control.

Cost-saving practices include:

- Using certified loading/unloading contractors

- Adopting safety management systems (SMS)

- Maintaining a clean claims history

- Avoiding high-risk ports or unstable regions

- Regularly reviewing charter party terms to minimize liability triggers

✅ Why this matters: A strategic approach to insurance not only protects your operations but also optimizes long-term costs. Partnering with experienced brokers and maintaining solid operational discipline are key levers for savings.

8.Common Claims Scenarios and Case Studies

Understanding real-world claims helps charterers grasp the practical importance of having liability coverage. Here are common situations where charterer liability insurance has proven essential.

Cargo Damage Due to Poor Loading

In one case, a time charterer hired a third-party stevedore to load grain. Improper distribution caused the cargo to shift during transit, damaging the hull and contaminating other shipments. The shipowner filed a claim for hull damage and demurrage losses due to delayed unloading.

Insurance covered:

- Hull repairs

- Cargo contamination claims

- Owner’s legal fees

Without liability coverage, the charterer would have faced over $300,000 in direct and legal expenses.

Pollution Fine After Bunker Spill

A charterer overseeing bunkering operations at a South Korean port was held liable for a bunker spill caused by a faulty connection. Authorities issued a $500,000 fine and required cleanup efforts.

The charterer’s policy covered:

- Cleanup operations

- Environmental fine (non-criminal)

- Public relations support and legal counsel

This highlights the necessity of having clear pollution coverage, especially in regions with strict marine environmental laws.

Delay Due to Port Congestion or Miscommunication

A voyage charterer booked a vessel to arrive at a congested port, without ensuring berth availability. The ship remained idle for six days, and the owner demanded demurrage compensation as per the charter party.

Charterer liability insurance covered:

- Demurrage cost

- Legal expenses in dispute resolution

- Partial off-hire liability

This case shows how communication and planning failures — even without physical damage — can lead to expensive claims.

Charter Party Disputes over Off-Hire Periods

A time charterer returned a vessel early due to cargo cancellation, citing force majeure. The shipowner challenged the claim and demanded off-hire payment and damages for breach of contract.

The insurer assisted with:

- Legal interpretation of force majeure clause

- Negotiation with the owner

- Partial compensation for off-hire claim

Without insurance, the charterer would have absorbed legal costs and the full claim payout — over $180,000.

✅ Why it matters: These scenarios illustrate how charterers face risks even when the vessel operates without incident. Claims are not limited to physical damage; contract missteps, scheduling errors, and regulatory misjudgments are all significant liabilities.

9.Charterer Liability Insurance in Different Jurisdictions

Marine laws and insurance obligations vary across regions. Charterers operating internationally must understand how jurisdiction affects liability exposure and compliance.

United States (Jones Act, COFR requirements)

In U.S. waters, charterers are subject to:

- The Jones Act: Governs the use of U.S.-built and -flagged vessels for domestic transport. Violations can incur penalties.

- COFR Requirements: Charterers must show financial capability to handle pollution incidents. A COFR certificate is mandatory and often requires proof of charterer liability insurance with sufficient pollution coverage.

European Union Regulations

The EU enforces strict environmental and safety protocols. Charterers face liabilities under:

- EU MRV (Monitoring, Reporting, and Verification) Regulation for carbon emissions

- Port State Control inspections

- Penalties for non-compliance with crew welfare and vessel safety standards

Failure to meet these obligations can lead to fines, detention, or blacklisting.

Asia-Pacific Maritime Law Considerations

Charterers operating in Asia must navigate:

- Local pollution laws (e.g., China’s strict discharge limits)

- Licensing rules for foreign charterers in Indonesian and Philippine waters

- Port authority rules that differ widely across Asia

Many countries also favor shipowners in legal disputes, making insurance even more crucial for charterers.

Role of ITIC, UK P&I Club, and Other Institutions

Several industry groups and mutual insurers provide guidance and coverage options tailored to charterers:

- ITIC (International Transport Intermediaries Club): Offers liability cover for transport professionals including charterers.

- UK P&I Club, Gard, Skuld: These mutuals provide charterer-specific coverage and legal resources.

- Lloyd’s Market: Often insures large operators through syndicates and bespoke policies.

✅ Why it matters: Operating in multiple regions means facing varied legal expectations. Charterer liability insurance can be tailored to meet both international compliance and local regulatory standards.

10.How to File a Charterer Liability Claim

Filing a claim under a charterer liability insurance policy requires prompt, precise action. Knowing the process in advance ensures better outcomes and faster resolution.

Initial Steps: Notification and Documentation

Once an incident occurs, the charterer should immediately notify their broker and insurer. Delays can compromise the validity of the claim.

Prepare and submit:

- Incident report (time, place, cause, parties involved)

- Charter party agreement and relevant clauses

- Photographic or video evidence, if available

- Third-party communications or complaints

Early transparency is key — even if the full scope of liability is unknown.

Working with Your Broker and Underwriter

The broker typically acts as the charterer’s first point of contact. They help compile documentation, liaise with underwriters, and manage expectations.

Their role includes:

- Explaining what’s covered and what’s not

- Coordinating communication between legal teams and insurers

- Assisting with form submissions and follow-ups

Engaging a marine-specialized broker accelerates the process and reduces back-and-forth.

Role of Legal Teams and Adjusters

Depending on the complexity, insurers may appoint claims adjusters and maritime legal advisors. These professionals:

- Investigate cause and extent of loss

- Assess whether policy terms apply

- Support charterers through legal proceedings if needed

Having a prepared legal team, ideally one already familiar with your operations, ensures smoother negotiations.

Typical Claim Processing Time and Payout

Timeframes vary based on claim complexity and responsiveness. Straightforward claims (e.g. fines, cargo loss) may settle within 30–60 days. Disputed charter party breaches or third-party injuries may take longer.

Insurers aim to resolve valid claims efficiently, but cooperation and documentation from the charterer play a major role.

✅Takeaway: Fast, accurate reporting backed by clear documentation is the foundation of a successful claim.

Charterer liability insurance is your safeguard against the financial and legal risks that come with chartering a vessel—from cargo damage and pollution fines to delay penalties and contractual breaches. Unlike P&I or Hull & Machinery cover, it’s designed specifically for charterers’ liabilities, filling critical gaps and ensuring peace of mind whether you’re on a single voyage or managing a fleet. By understanding policy scope, exclusions, and cost drivers—and by partnering with experienced brokers—you can secure the right protection and keep your operations running smoothly.

Ready to protect your chartering operations?

📞 Contact Arctic pandi today to discuss tailored charterer liability solutions and get a free risk assessment. Ensure you’re covered before your next voyage!

Q1: Do I really need charterer liability insurance if the ship has P&I coverage?

Yes. P&I insurance protects the shipowner — not the charterer. You need separate coverage for your own liabilities.

Q2: What does charterer liability insurance actually cover?

It covers damage to the vessel, cargo issues, pollution, demurrage, and legal claims caused by the charterer’s actions.

Q3: How much does this insurance typically cost?

Costs vary, but most charterers pay between $7,000 and $50,000 per year based on risk level and vessel type.

Q4: What happens if I don’t have this insurance?

You may be personally liable for millions in damages or legal costs — especially in cargo loss, delays, or accidents.